admin

Updated June 23, 2026

13 min read

Key Takeaways

|

Yes, you may qualify for disability benefits after a workplace injury if your condition prevents you from working and meets the requirements of programs such as SSDI, SSI, or workers’ compensation. Being sidelined by an injury can be stressful, especially if you’ve been out of work for months, your medical bills are piling up, and workers’ compensation alone isn’t enough.

These challenges are common, and according to the U.S. Department of Labor, only 41.9% of working-age people with disabilities participate in the labor force, compared to 78% without disabilities, emphasizing the long-term impact of workplace injuries.

In this guide, you’ll learn whether you qualify, which benefits may apply to your situation, when and how to file your claim, what to expect in approval timelines, potential benefit amounts, and the mistakes many injured workers make that can delay or reduce their benefits.

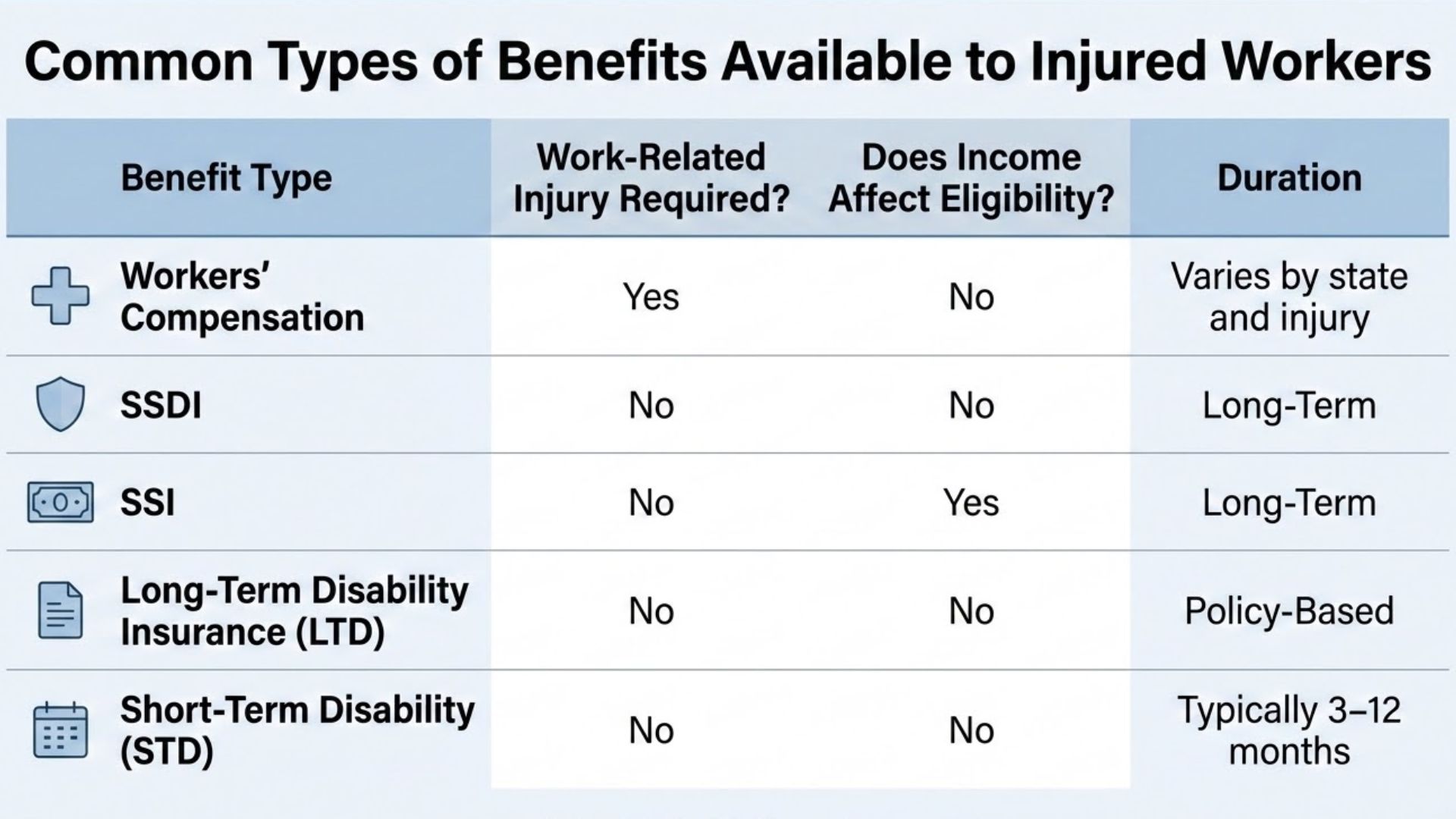

What Types Of Disability Benefits Are Available After A Workplace Injury?

A workplace injury doesn’t limit you to workers’ compensation alone. Depending on your medical condition, work history, income, and insurance coverage, you may qualify for multiple disability programs at the same time.

Workers’ compensation is often just the first source of support. If your injury prevents you from working for an extended period, other programs may also provide financial assistance while you recover or adjust to long-term limitations.

Workers’ Compensation

Workers’ compensation provides financial and medical support if you’re injured or become ill on the job. Depending on your state, it can cover medical bills, rehabilitation, and a portion of lost wages to help you recover without bearing the full financial burden.

Social Security Disability Insurance (SSDI)

SSDI is a federal program for workers who have paid into Social Security. You may qualify if a medical condition prevents substantial work for at least 12 months. It provides long-term income support while protecting your financial future.

| Substantial Gainful Activity (SGA) Limits – 2026 The Social Security Administration (SSA) uses Substantial Gainful Activity (SGA) limits to determine whether your earnings qualify as disability-level income. These limits are updated annually to reflect changes in national wage levels. For 2026, the monthly SGA limit is $1,690 for non-blind individuals and $2,830 for individuals who are statutorily blind. If your earnings exceed these limits, you may not qualify for SSDI benefits, even if you have a medical condition. |

Supplemental Security Income (SSI)

SSI offers financial assistance to individuals with disabilities who have limited income and resources. Unlike SSDI, eligibility is based on need rather than work history, helping those who may not have enough work credits to qualify for SSDI benefits.

Long-Term Disability Insurance

Long-term disability insurance, often provided by employers, replaces a portion of your income if you cannot work due to illness or injury. Coverage varies by policy, but it helps you maintain financial stability while recovering or adapting to long-term disability.

Short-Term Disability (STD)

Short-Term Disability insurance provides temporary income replacement if a medical condition prevents you from working. Coverage is often available through an employer-sponsored plan or a private policy. Unlike workers’ compensation, the injury does not have to be work-related to qualify. Because Social Security Disability Insurance approvals can take several months, STD benefits may help bridge the financial gap during recovery.

| Quick Tip: If you’re unsure which benefits apply to your situation, start by reviewing your work history, insurance coverage, and medical records. These factors often determine which programs you may be eligible to receive. |

Does Workers’ Compensation Automatically Qualify You For SSDI?

No, getting workers’ compensation benefits does not automatically mean you’ll qualify for SSDI. Although both programs help people who can’t work because of an injury or medical condition, they have different requirements.

Workers’ compensation looks at whether your injury happened because of your job. Social Security Disability Insurance looks at whether your condition prevents you from working for at least 12 months, no matter how or where the injury occurred.

SSDI vs. Workers’ Compensation: What’s the Difference?

| Factor | SSDI | Workers’ Compensation |

| Administered By | Social Security Administration (SSA) | State Workers’ Compensation Programs |

| Requires a Work-Related Injury | No | Yes |

| Disability Must Last 12+ Months | Yes | Not Always |

| Work Credits Required | Yes | No |

| Covers Non-Work Injuries | Yes | No |

| Quick Tip: Don’t assume your workers’ compensation paperwork will be enough for SSDI. The SSA may require additional medical evidence, treatment records, and documentation showing how your condition affects your ability to work daily. |

Which Pays More: SSDI Or Workers’ Compensation?

It depends on your work history, the severity of your injury, and the state you live in. Both Social Security Disability Insurance and workers’ compensation provide financial support, but they work differently and are calculated in different ways.

How Social Security Disability Insurance Works

- Payments are based on your past earnings and how much you’ve contributed to Social Security over your lifetime.

- SSDI benefits may be taxable, depending on your total income.

- Once approved, SSDI is usually long-term, continuing as long as your disability persists.

- Family members may also qualify for benefits in some cases.

How Workers’ Compensation Works

- Payments are based on your injury and lost wages due to that specific work accident.

- Benefits are generally not taxable.

- Duration and amounts vary by state and the type of disability (temporary or permanent).

- Family benefits are usually not included, except in cases of fatal injuries.

Here is a quick comparison table to help you understand better:

| Feature | SSDI | Workers’ Compensation |

| Payment Basis | Earnings History | Injury and Wage Loss |

| Taxable | Sometimes | Usually Not |

| Duration | Potentially Long-Term | State Dependent |

| Family Benefits Available | Yes | Usually No |

When Should You Apply For Disability Benefits After A Workplace Injury?

You should apply as soon as it becomes clear that your injury will prevent you from working for at least 12 months. Waiting too long can delay benefits and back pay you may be entitled to.

Disability Claim Timeline

| Stage | Typical Time |

| Workplace Injury Occurs | Day 1 |

| Workers’ Compensation Claim Filed | Days 1–30 |

| Medical Evidence Collection | Months 1–3 |

| SSDI Application Submitted | As Soon as Disability Is Expected to Last 12 Months |

| SSDI Waiting Period | 5 Months |

| Initial Decision | 3–8 Months |

Did You Know About the 5-Month SSDI Waiting Period?The Social Security Administration has a mandatory 5-month waiting period, meaning benefits are not paid for the first five months of your disability. However, the SSA provides retroactive benefits (lump-sum back pay) for up to 12 months before your application, as long as your disability onset date is verified. Why This Matters

|

What Can You Do While You Wait?

Waiting for a disability decision can be stressful, especially if you’re dealing with lost income and ongoing medical expenses. The reassuring part is that there are several forms of support you can explore while your Social Security Disability Insurance claim is being reviewed.

SNAP and Public Assistance

If groceries and household expenses are becoming difficult to manage, check whether you qualify for the Supplemental Nutrition Assistance Program (SNAP) or other state assistance programs. Your local Department of Social Services may also offer emergency financial assistance, utility assistance, or cash benefits depending on your situation.

State Temporary Disability Programs

Some states offer temporary disability benefits for individuals who are unable to work because of a medical condition or injury. These programs can provide short-term income replacement while you wait for a disability decision. Eligibility requirements vary by state, so it’s worth checking what options are available where you live.

For example, if a warehouse worker in Texas injures their shoulder while lifting heavy boxes and cannot work for 3–4 months, they may qualify for the state’s temporary disability program, which replaces a portion of their lost wages while they recover and wait for long-term disability approval.

Community and Non-Profit Resources

Local organizations can often provide help when finances become tight. By calling 2-1-1, you can connect with community resources, including programs run by United Way, that may offer assistance with rent, utility bills, food, transportation, or other essential needs. Many people overlook these programs, but they can make a meaningful difference during a difficult period.

Medicaid Coverage

Medical treatment doesn’t stop just because you’re waiting for benefits. Applying for Medicaid may help ensure your doctor visits, medications, hospital care, and rehabilitation services remain covered. Continuing treatment is not only important for your health, but it can also help strengthen your disability claim by creating ongoing medical documentation

What Medical Evidence Do You Need For A Disability Claim?

To win a disability claim, you must demonstrate that your injury or medical condition is severe, well-documented, and limiting enough to affect your ability to earn a living. This requires detailed medical records, physician evaluations, treatment history, and evidence of ongoing functional limitations.

When preparing your claim, gather as much relevant documentation as possible, including:

- Medical records& Physician notes: Document your diagnosis, symptoms, treatment progress, and how your condition affects daily functioning.

- Diagnostic imaging: Provides objective evidence through X-rays, MRIs, or CT scans that support your injury.

- Treatment history & Medication records: Shows ongoing medical care, prescribed treatments, and efforts to manage your condition.

- Work restrictions & Rehabilitation records: Explain physical limitations, recovery progress, and activities you can no longer safely perform.

- Hospital discharge summaries: Summarize hospital treatment, procedures performed, diagnoses, and recommendations for continued care afterward.

What Are Your Chances of Getting Approved? Your approval depends on the strength of your medical evidence, the severity of your injury or illness, and whether your condition meets Social Security’s definition of disability. While no one can guarantee approval, understanding the above factors can increase your odds and make the process smoother. |

What Happens After You Submit Your Disability Application?

Once your application is in SSA’s hands, it enters a detailed review process. Basically, SSA wants to make sure your medical condition and work history support your claim.

Here’s what usually happens:

- Application Received: SSA checks your forms to make sure everything is complete.

- Medical Evidence Review: Your doctor’s notes, test results, and treatments are assessed.

- Requests for More Info: Sometimes, they need additional records or clarification from your doctors.

- Consultative Exam (if needed): A SSA-appointed doctor may examine you to confirm your condition.

- Decision: SSA will approve or deny your claim. If denied, you can appeal.

Quick Tip: Answer any SSA requests as soon as possible. The faster you respond, the faster your claim moves.

How Much Could You Receive in Disability Benefits?

The amount you may receive in disability benefits depends on your work history, earnings record, and the type of disability program you qualify for, like SSDI, SSI, or workers’ compensation.

Understanding your potential benefit helps you plan your finances and reduces uncertainty during the application process.

Factors That Affect Your Benefits

- Lifetime Earnings

SSDI payments are based on your average earnings over your working life. The higher your past income, the higher your potential benefit.

So, how can you calculate this? Let’s have a look

- Find your average monthly earnings (AME) – Add up your past yearly earnings, divide by the total number of months worked.

- Apply simple SSDI percentages:

- 90% of the first ~$1,300 of AME

- 32% of the portion between ~$1,300 – ~$8,000

- 15% of any amount above ~$8,000

- Add them together – This gives your rough monthly SSDI benefit.

- Adjust for offsets – If you receive workers’ compensation, SSA may reduce your SSDI by a portion of that payment.

For example, if your average monthly earnings were around $4,000, your SSDI benefit could be roughly $2,400 per month.

Average monthly earnings = $4,000

90% of the first $1,300 = $1,170

32% of the remaining $2,700 = $864

Estimated SSDI = $1,170 + $864 = $2,034/month

If you also get $500/month workers’ comp: $2,034 − $500 = $1,534/month total income

Tip: This is just an estimate. You can check your Social Security Statement online or use the SSA calculator for a more precise number.

- SSDI Work Credits: To qualify for SSDI, you need enough work credits. These credits come from the number of years you worked and paid Social Security taxes.

- Workers’ Compensation Payments: If you are receiving workers’ comp, it may reduce your SSDI benefits because of offset rules.

For example, if Sarah gets $1,000/month from workers’ comp and her SSDI calculation is $2,000, then SSA may reduce her SSDI to $1,500 to account for the workers’ comp offset.

- Other Disability Income: If you receive other disability income (like long-term disability insurance), it can impact your total monthly benefit.

Why Disability Claims Are Denied

Many disability claims are denied because the Social Security Administration (SSA) does not have enough medical proof, the application is incomplete, or the applicant does not meet strict eligibility rules.

A large number of claims are rejected at the initial stage. In fact, around 60%-70% of initial disability applications are denied, according to SSA workload data. However, this doesn’t mean you are ineligible; it often means more documentation or stronger medical evidence is needed.

Here are the most common reasons:

- Insufficient Medical Evidence

Many claims are denied when medical records don’t clearly show how severe the condition is or how it limits work ability. The Social Security Administration needs consistent, detailed, and objective medical documentation.

- Procedural & Administrative Errors

Simple mistakes like missing forms, incorrect information, or incomplete sections can lead to denial. Even small administrative errors can delay processing or result in rejection of the disability claim.

- Non-Compliance with Treatment

If you don’t follow prescribed treatment or skip doctor visits, SSA may assume your condition is not severe or could improve with proper care, affecting your eligibility for benefits.

- Working and Earning Too Much

If your income exceeds SSA’s Substantial Gainful Activity (SGA) limit, your claim may be denied because you are considered capable of performing significant work despite your disability.

- Inconsistencies and Surveillance

Differences between your statements, medical records, or reported activities can hurt your claim. The Social Security Administration may also use surveillance or reviews to verify if your daily activities match your reported limitations.

Can You Work While Receiving Disability Benefits?

Yes, but only in a limited way. You may be able to do some part-time work under certain disability programs, but earning above specific income limits can reduce or even stop your benefits.

What You Need to Know?

Many people assume that once they apply for disability benefits, they must completely stop all work. That’s not always true. However, the Social Security Administration (SSA) has strict rules about how much you can earn while still being considered “disabled.”

| Work Type | What Happens |

| Light / Part-Time Work | Maybe allowed if earnings stay low |

| Trial Work Period (SSDI) | Temporary work allowed without immediate penalty |

| Regular Full-Time Work | May lead to termination of benefits |

What You Should Do Next

A workplace injury can leave you unsure about your health, income, and future, but you don’t have to navigate the disability process alone. Understanding your options for workplace accident disability benefits is the first step toward securing the support you may be entitled to and avoiding delays in your claim.

If you’re still unsure whether you qualify or need help with your disability claim after an accident, the team at Nationwide Disability Representatives can guide you through the process and help you take the right next steps with confidence.